What is Total Insurable Value (TIV)?

Total Insurable Value is a term used in insurance to describe the total value of every asset that is covered under the insurance package. These assets include everything from furniture and machinery to land and buildings.

ALSO READ ABOUT What is Corporate Insurance? 5 Steps to Select the Perfect Insurance Plan

How Does TIV Work?

When you invest in an insurance policy, you have to pay the insurance company to secure the insurance; this money is known as a premium. The premium amount depends on the TIV, a higher TIV means a more expensive premium and vice versa. This is because the more expensive asset you are trying to secure, the more the insurance company will have to pay.

Suppose your firm had an accident like a fire or theft, and your total insurable value will be used to determine how much you will receive as compensation to replace or repair your damaged assets.

Example of Total Insurable Value

Suppose you own a boutique.

Shop value: $200,000

Furniture: $30,000

Inventory (On display and off-display clothes): $50,000

Your Total Insurable Value would be:

$200,000 (Shop Value) + $30,000 (Furniture) + $50,000 (Inventory) = $280,000

As your TIV is upto $280,000, in case of any accident in your shop, you can receive compensation of upto $280,000 to help you rebuild or replace your assets.

Why Is TIV Important?

From a business perspective, understanding your Total Insurable Value is crucial. It ensures that you are fairly compensated in the event of a loss. By comparing your TIV with the insurance payout, you can verify the fairness of the compensation. By knowing your TIV, you can avoid this risk and make sure you have enough coverage to protect all your assets.

How TIV Affects Your Insurance Premiums

A higher TIV means a higher insurance premium for full coverage. The higher premium is worth protecting all your assets in case of adversity; it ensures you can easily repair or replace them if needed. You might save money on premiums without enough coverage, but you could face a big financial loss if something happens to your property.

How to Calculate TIV

- Real Estate Value: Evaluate the firm’s property to calculate its market price. These include the firm’s building, land, or any other real estate property that is to be insured.

- Equipment and Furniture: List all the equipment the firm owns, including its machinery, furniture, and other physical assets. Each item is valued based on its current worth.

- Inventory: Add up the total value of all the inventory you have. This includes everything you keep in stock to sell or use in your business, like raw materials or finished goods.

- Business Interruption Costs: Consider how much it would cost you if your business stopped operating for a while. This might include ongoing expenses like rent, employee salaries, and utility bills.

Once you have evaluated and calculated the value of all these assets, you can add them up, and that will be your firm’s Total Insurable Value.

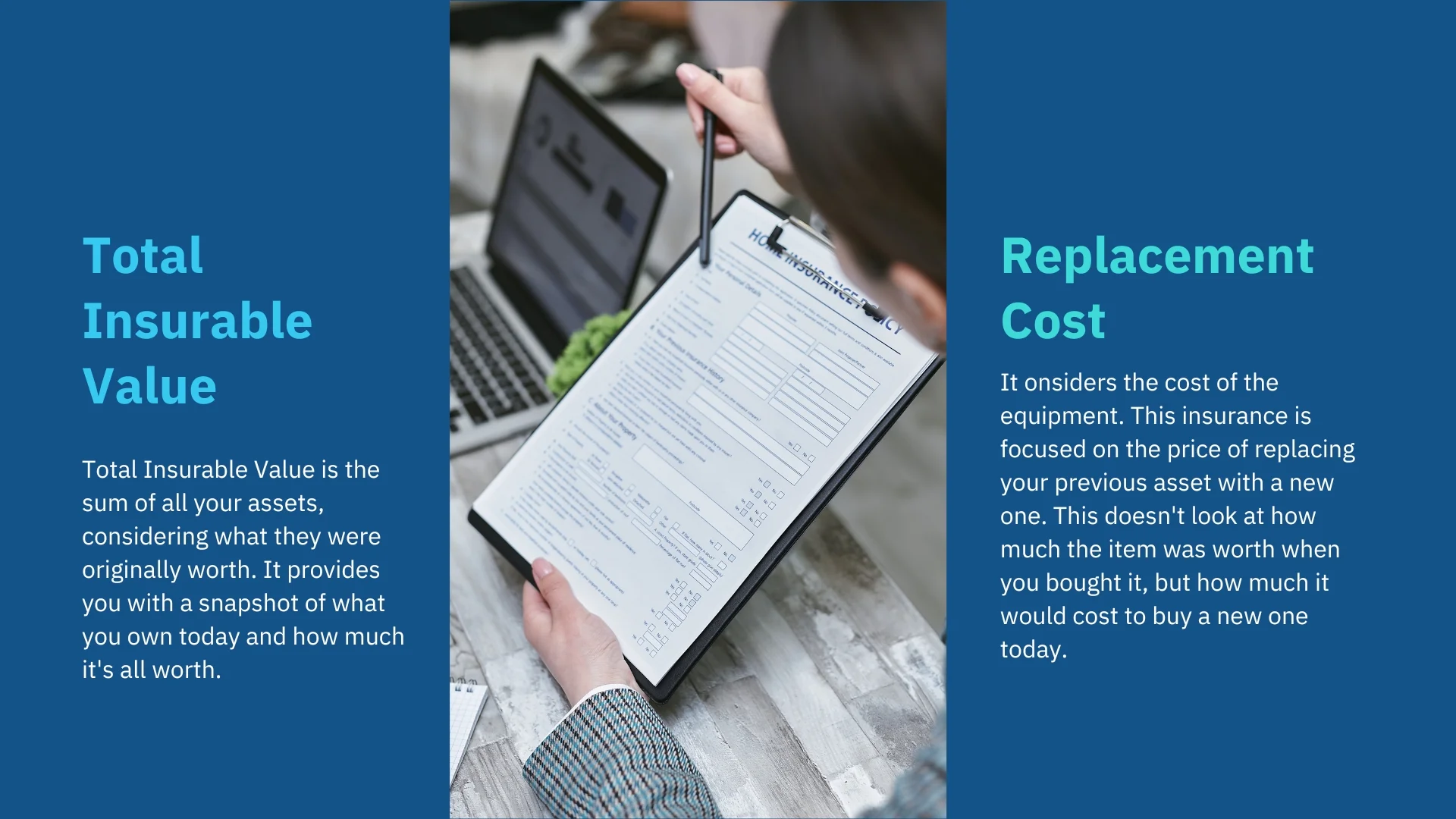

TIV vs. Replacement Cost: What’s the Difference?

- Total Insurable Value is the sum of all your assets, considering what they were originally worth. It provides you with a snapshot of what you own today and how much it’s all worth.

- Replacement Cost considers the cost of the equipment. This insurance is focused on the price of replacing your previous asset with a new one. This doesn’t look at how much the item was worth when you bought it, but how much it would cost to buy a new one today.

For example, let’s say you bought a machine worth $25,000 three years ago. The TIV for the machine will be $25,000, but the replacement cost of that machine will depend on the current market of that machine. It could be higher or lower depending on the market trends.

Tips for Managing Your TIV

- Regular updates are key to managing your Total Insurable Value effectively. As the value of your assets can change over time, it’s important to keep your records current. This proactive approach ensures that your insurance policy reflects the true value of your assets, providing you with comprehensive coverage.

- Professional appraisals play a crucial role in managing your Total Insurable Value. By obtaining accurate valuations for your property and high-value items, you can be confident that your TIV is calculated correctly.

- Review Your Coverage: Review your insurance policy at least once a year to make sure your TIV is still accurate and that you’re not underinsured.

Final Statement

Understanding TIV helps you protect your property and assets with the right amount of insurance coverage. By calculating your TIV correctly, you can ensure that you’re fully covered in case of an accident or disaster. Comparing TIV with replacement cost can also help you decide which type of insurance coverage is best for you.

Whether you’re insuring a home, a business, or other valuable property, knowing your TIV will help you make the right choices to protect what’s important to you.

ALSO READ ABOUT 5 Important Difference Between Life and Health Insurance

FAQs

What does TIV mean in insurance?

Total Insurable Value is a term used in insurance to describe the total value of every asset that is covered under the insurance package. These assets include everything from furniture and machinery to land and buildings.

What is the difference between ITV and TIV?

ITV (Insured to Value) refers to how closely the insurance coverage matches the actual value of the insured property, ensuring it’s neither underinsured nor overinsured. TIV (Total Insurable Value), on the other hand, is the total worth of all assets covered under an insurance policy.