In a world where financial literacy and management are given utmost importance, where every next video you see is about how to save, invest, or create more wealth, where should you start? What should you do with your next paycheck? And most importantly, whose ideas should you follow?

We are here with a 7-step financial order of operations that are designed to help you figure out what to do with your every paycheck, how to create all of those things you see in those finance videos and get financially independent and free.

READ MORE 5-Step Personal Finance Flowchart for Beginners

What is the Financial Order of Operations?

The financial order of operations is a strategy that helps prioritize financial actions in a proper order that ensures financial growth. It’s like a step-by-step guide that dictates how you should go on with your finances.

A financial order of operations helps us stay on track, properly prioritize money matters, eliminate extras, and improve the strategy continuously. Without a proper order, we will start assigning the budget as we see fit, not based on proper facts. We might overspend on savings or daily needs, ignoring other important plans, but that is where having a financial order of operations comes in handy. It helps you set up a strategy that assigns your budget according to your needs and goals.

The interesting thing about us is that more than 65% of people don’t have a rigid financial plan for their future. Most of us just wing it every month when the paycheck comes. We pay the bills as they come, without any plan. Where do you think this will lead to? A point where you will have to take loans for unexpected expenses, and again and again till you don’t have enough credit score and you are stuck in a debt trap. So, make sure you follow the 7-step financial order of operations below to avoid such a fate.

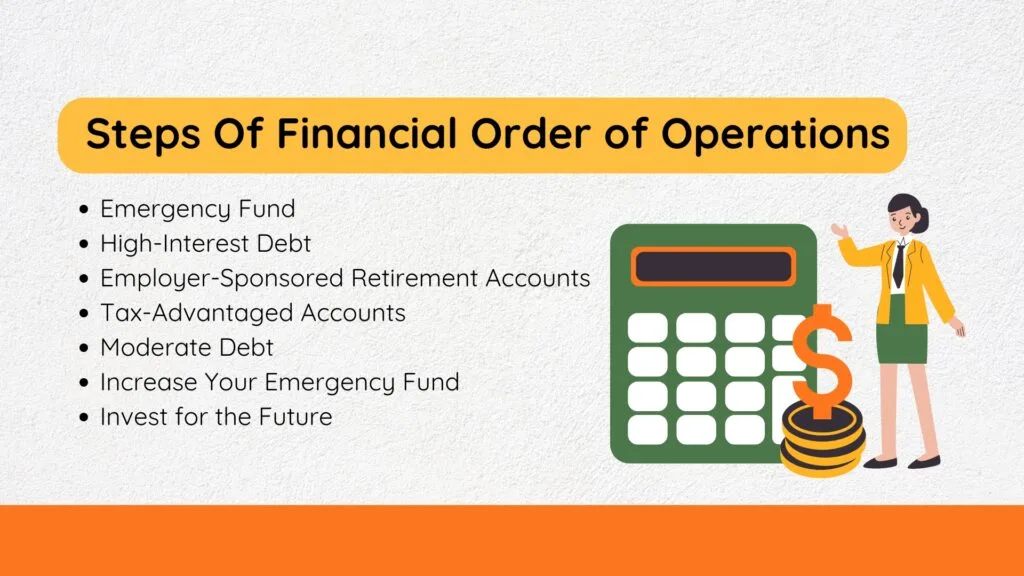

Step-by-Step Breakdown of the Financial Order of Operations

Step 1: Build a Financial Safety Net (Emergency Fund)

The most important step of any good plan is contingency, and that’s where we start by focusing on building a safety net for uncertain times. An emergency fund is the savings and wealth set aside that can be liquidated into cash quickly whenever needed during a financial crisis.

The goal while investing in emergency funds is that the amount should be enough to cover all your current expenses for at least 3 months to 6 months. The amount should cover the same amount you spend every month now, including your extra expenses like dining out. The goal of having an emergency fund is to make sure you don’t need to depend on other sources during times of need. Since it’s an emergency fund, you must ensure it’s accessible when required.

Tip: You can start saving some amount in a high-interest-yielding savings account that provides your better interest income.

Step 2: Pay Off High-Interest Debt

Once you have the specifics for your emergency funds, it’s time to counter the money drainer – Debts. Debts refer to the amount you have borrowed from others, whether it’s a credit card, bank loans, private loans, or even just a friend. It’s the amount that you have to pay back, which means till you have zero debt obligations, you won’t have enough to invest at other places.

Two methods to take on debt obligations are the avalanche and the snowball techniques. In the avalanche approach, you write down all obligations from the top to the bottom, with the debt with the highest interest rate at the top. Essentially, you start prioritizing high-interest debts to reduce the extra charges quickly and then move to the next one with the highest charges.

In the snowball method, you start off with the smallest loan, meaning if your lowest debt obligation is $1000, you prioritize paying it off and then move on to the next one. The method is designed to reduce stress and slowly attack debt with a slow start. For instance, you begin paying a specific amount, say $1000 monthly, for your lowest loan. Once paid, you move to the next debt, pay the debt fees for the following loan, and add the amount you paid on the first debt, thereby increasing your ability to pay the debt.

Step 3: Max Out Employer-Sponsored Retirement Accounts (401(k), 403(b))

If you are working at a place that offers retirement plans like 401k or the 304b plan with the option of a match, don’t miss out on the chance. A match is where you have to contribute a little from your payment, and your firm takes care of the rest. It provides an excellent retirement savings plan; all you have to do is ensure that you take advantage of it by paying the maturing amount.

Here’s how it works: let’s say your firm offers a 100% match on the first 5% of your salary you pay. This means that if you pay the principal amount, which is 5% of your salary, the employer will add the remaining 95% to your retirement account. Basically, with 5% of your income, you get extra money in your retirement account that will grow tax-free. You have no downside; if you don’t do it, you are simply denying your future self a better retirement amount.

READ MORE 8 Important Steps for Personal Finance for Beginners

Step 4: Tax-Advantaged Accounts (IRAs, HSAs, etc.)

Let’s first look at what tax-advantaged accounts are. A tax-advantaged account is a bank account that is not taxed, so people can put their savings and investment amounts in it without worrying about getting it taxed. These accounts are designed for people who want to save or invest for their future without further taxing their income. The deal here is that you invest and keep the amount in the bank’s account, and they offer you a tax-exempt account where the amount will grow with time.

They can be accessed in various ways, such as one sponsored by your employer, such as 401(k) or 403(b). These accounts sponsored by employees are funded directly by your company. That means the employer credits a percentage of your earnings to your tax-advantaged savings account. The rest will be transferred to your account for salary, eliminating the need to transfer the money manually.

In the same way, IRA (Individual Retirement Account) accounts also provide similar benefits. However, you must transfer the money you wish to save or invest it manually. Additionally, accounts such as the HSA (Health Savings Account) are extremely helpful in dealing with medical emergencies. The amount you deposit into this account and the interest you earn isn’t tax-deductible as the money is saved to help in medical emergencies.

Step 5: Pay Off Moderate Debt

Once you finish the above section, you can move towards middle-level debt obligations. These are the more manageable loans, like student loans, car payments, or any other loan with an interest rate below 10%.

With high-interest debts out of the way, these debts can really eat up your cash and make your finances tight for the moment. With these debts paid off, you will likely have more cash on hand, providing higher financial flexibility.

So, there are a few things you should consider during this phase. Even though the debt is not as pressing as high-interest debts, don’t pause the payment or ignore them; use the debt avalanche or snowball method to continue paying off your debts. Most importantly, just because you are freeing up some of your financial strains, it doesn’t mean you should opt for more, so avoid buying new things until you are financially comfortable.

Step 6: Increase Your Emergency Fund

The general rule for an emergency fund is to save upto three to six months worth of your monthly expense for emergencies where you won’t receive any money, whether because of situations like covid or job loss. These funds are your backup cave where you can hibernate during tough times without worrying about money. But as per the financial order of operations, we are to think beyond it.

The general rule says to save for three to six months, but you have to consider more things when it comes to personal planning. If you are planning to do some serious life-altering things like starting a new business, planning a child, or being the only source of income in the house, you have to consider building up a larger emergency fun pool, which can extend the savings for up to nine to twelve months.

To get started with the emergency fund, decide how much income you can afford to allocate to this account. You manually transfer or automate the transfer after you receive your income for better surety. You can also use the windfall strategy, where the extra amount you receive as a gift, as a tax return, or any other amount of cash is deposited in your emergency account.

Step 7: Invest for the Future

The last step of the financial order of operations is to invest. Investing is a step that helps you build wealth for the long term, whether it’s investing in stocks, mutual funds, FD, or real estate. Investing while paying off your debts can be challenging, but it is not impossible. You can start off by investing a small amount. Once one of the debts is paid off, you can divide the amount you were paying for the debt and start using it for saving and investment purposes.

The only thing you have to ensure while investing is that you are consistent, meaning you invest every month and increase the amount as you get more space in your budget.

READ MORE Why Is Personal Finance Dependent Upon Your Behavior?

Frequently Asked Questions (FAQs)

What is step 7 of the financial order of operations?

Here are the 7 steps of the financial order of operations:

Emergency Fund

Paying Off High-Interest Debt

Take Advantage of Employer Matches

Invest in Tax-Advantaged Accounts

Pay Off Moderate Debt

Increase Your Emergency Fund

Invest for the Future

What is the Foo method of finance?

The financial order of operations is a strategy that helps prioritize financial actions in a proper order that ensures financial growth. A financial order of operations helps us stay on track, properly prioritize money matters, eliminate extras, and improve the strategy continuously.